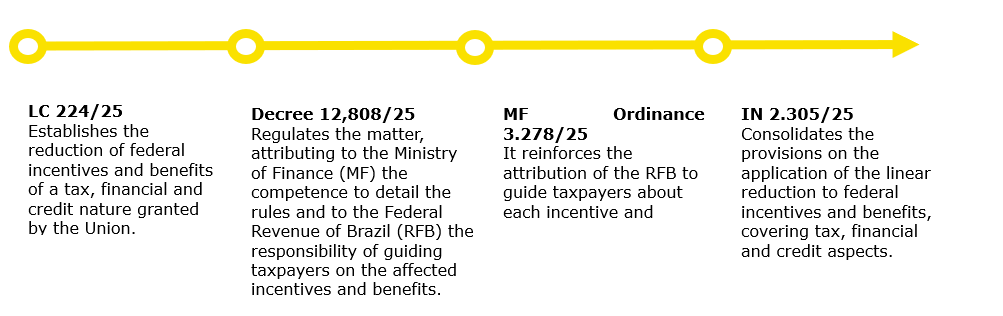

At the end of December 2025, Complementary Bill 128/25 (PLP 128/25) was converted into Complementary Law 224/25 (LC 224/25). Subsequently, its regulation was enacted through Decree 12,808/25, later complemented by Ordinance MF 3,278/25 and Normative Instruction RFB 2,305/25 (IN 2,305/25).

Together, the four regulations establish guidelines for the reduction of federal incentives and benefits of a tax, financial and credit nature, applicable exclusively within the scope of the Union, with important impacts for both individuals and legal entities.

In this article, we highlight the main guidelines on the granting and reduction of tax benefits and incentives brought by the aforementioned regulations.

Sequence and theme of the regulations

Granting or changing new tax benefits and incentives

LC 224/25 establishes that bills that grant, expand or extend tax incentives or benefits, including tax deferrals (except those that imply the postponement of the payment of the tax), in general, must present:

- estimation of the number of beneficiaries;

- term limited to five years (except benefits linked to long-term investments);

- objective and measurable performance targets in the economic, social and environmental dimensions;

- impact on the reduction of regional inequalities, when applicable; and

- mechanisms for transparency, monitoring and evaluation of results in relation to the established goals.

Reductions – scope

LC 224/25 also provides for the reduction of incentives and benefits applicable to federal taxes (PIS, Cofins, IRPJ, CSLL, IPI, II and social security contribution), provided that they are itemized in the statement of tax expenditures referred to in paragraph 6 of article 165 of the Federal Constitution (CF/88) attached to the Annual Budget Law (LOA) of 2026 or have been instituted through the following regimes:

- presumed profit;

- Special Regime for the Chemical Industry (Reiq);

- presumed IPI credit;

- presumed PIS and Cofins credit for various sectors, in accordance with the applicable Mercosur Common Nomenclature (NCM) – such as regular intercity (except metropolitan) and interstate road passenger transport, goods of animal or vegetable origin, vegetable flours and oils, pharmaceuticals, citrus and coffee;

- reduction to zero of PIS and Cofins rates, including on imports, for domestic sales of agricultural and agricultural products, according to the applicable NCM – such as fertilizers, seeds and seedlings, flour, groats, meals, crushed or flake grains, pasta and beef, pork, sheep, goat and poultry; and

- reduction of PIS and Cofins rates for petrochemical naphtha intended for the production or formulation of gasoline or diesel.

Reductions – standard taxation system

Regarding the reduction of tax incentives and benefits, according to LC 224/25, the standard taxation system to be considered is:

- IRPJ and CSLL – the rules that govern taxation by actual profit, without the application of discounts or tax benefits.

- IPI – the rules that establish the application of the rates contained in the Table of Incidence of the Tax on Industrialized Products (Tipi), disregarding reductions of any nature provided for in the Complementary Notes of Tipi.

- PIS and Cofins – the rules that establish the application of the following rates on revenue:

- 65% and 3%, in the cumulative calculation regime; or

- 65% and 7.6%, in the non-cumulative calculation regime.

- PIS-Import and Cofins-Import – the rules that establish the application of the following rates on the calculation basis provided for in article 7 of Law 10,865/04:

- 65% and 7.6%, in the case of imports of services; or

- 1% and 9.65%, in the case of importation of goods.

- II: the rules that establish the application of the rates contained in the Common External Tariff (TEC) or rates amended based on paragraph 1 of article 153 of the CF/88.

- Social Security Contribution: the rules that establish as a basis for calculation the total remuneration paid or credited, in any capacity, during the month, to insured employees, entrepreneurs, independent workers and self-employed service providers.

Reductions – forms of implementation

LC 224/25 also provides that the reduction will be implemented cumulatively as follows:

- Exemption and zero rate – application of a rate corresponding to 10% of the rate of the standard taxation system. It should be noted that the rates instituted in substitution of the exemptions cannot be changed by the Federal Executive Branch. In addition, under the terms of paragraph 7 of article 4 of the LC, the application of this additional rate does not confer on the purchaser of goods or services the right to appropriate credits. According to the legislation in force, the appropriation of these credits would be prohibited due to the exemption or the zero rate.

- Reduced rate – application of a rate corresponding to the sum of 90% of the reduced rate and 10% of the rate of the standard taxation system.

- Reduction of the calculation basis – application of 90% of the reduction of the calculation basis provided for in the specific legislation of the benefit.

- Financial or tax credit, including presumed or fictitious credit – use limited to 90% of the original value of the credit, canceling the unused amount. It should be noted that the new rule does not apply to credits already booked or whose right to bookkeeping has been acquired until December 31, 2025.

- Reduction of tax due – application of 90% of the tax reduction provided for in the specific legislation of the benefit.

- Special or optional favored regimes in which taxes are charged as a percentage of gross revenue – an increase of 10% in the percentage of gross revenue.

- Taxation regimes in which the calculation basis is presumed – 10% increase in the presumption percentages.

For legal entities taxed on the basis of presumed profit, LC 224/25 provides that an increase of 10% must be applied to the presumption percentages provided for in the IRPJ and CSLL legislation. This increase will be applied exclusively to the portion of total gross revenue that exceeds R$ 5 million in the calendar year, observing:

- the proportional application of the limit in each calculation period, with the possibility of adjustment in subsequent periods of the same calendar year; and

- the proportional application of the increase to the revenues of each activity.

Global limitation

A limitation of the total value of tax incentives and benefits was established. If the total amount exceeds 2% of GDP, the granting, expansion or extension of tax incentives and benefits is prohibited.

Exceptions

According to paragraph 8 of article 4 of LC 224/25, the reduction of incentives and benefits does not apply to:

- suspension of the tax in which there is only a temporal deferral in the payment of the tax;

- Manaus Free Trade Zone and Free Trade Areas;

- zero rate of the national basic food basket granted by Complementary Law 214/25 (LC 214/25);

- Prouni;

- Minha Casa, Minha Vida;

- Social Security Contribution on Gross Revenue (CPRB);

- constitutional immunities;

- industrial policy benefits for the information and communication technology sector and the semiconductor sector;

- benefits granted for a fixed period to taxpayers who have already fulfilled an onerous condition for their enjoyment;

- benefit enjoyed by a non-profit legal entity;

- ad rem rates;

- tax offsets for the assignment of free hours; and

- differentiated and favored treatment for micro and small companies.

Support for taxpayers

Pursuant to paragraph 9 of article 4, the Federal Revenue Service of Brazil (RFB) will provide a priority service channel to guide taxpayers on the application of the legislation, including exceptions to the linear reduction of benefits. This service will take place through the Receita Soluciona service, established by RFB Ordinance 446/24.

Validity

According to item "a" of item I of article 14 of LC 224/25, in cases that may result in an increase in the tax burden, the application of the law will occur from the first day of the fourth month following its publication – that is, from December 26, 2025 – in respect of the principle of nonagesimal anteriority.

The other changes brought by LC 224/25 came into force on January 1, 2026.

Article 3 of MF Ordinance 3,278/25 establishes that the reductions in incentives and benefits related to IRPJ and II will be implemented as of January 1, 2026, while the reductions applicable to other taxes will begin on April 1, 2026. It should be noted that IN 2,305/25 also recognizes the need to obey the nonagesimal anteriority for other taxes, in addition to IRPJ and II.

Points of attention

It is important to highlight that the limits of scope of LC 224/25 raise interpretative doubts. The exact definition of the incentives and benefits not achieved by the reduction is the subject of discussion. Therefore, a detailed analysis is recommended to identify which regimes remain preserved and which may be adjusted according to the criteria of limitation and reduction foreseen.

The apparent prohibition on the use of credits at the rate corresponding to 10% in cases of exemption and zero rate also raises doubts, especially considering import operations (governed by Law 10,865/04) and the principle of non-cumulativeness of PIS, Cofins and IPI.

The new rules do not automatically apply to the Contribution on Goods and Services (CBS) and the Tax on Goods and Services (IBS), instituted by the Tax Reform, since these taxes have their own regulations.

The new legislation specifically deals with the reduction of benefits linked to current federal taxes (such as PIS/Cofins, IPI, II, IRPJ) even if considered in the LOA, making no reference to Constitutional Amendment 132/23 (EC 132/23), nor to LC 214/25.

Our tax team is prepared to advise clients throughout the adaptation period, offering technical and legal support for the implementation of changes resulting from the new tax rules.